Why is AML important?

Anti-money laundering legislation is a vital component to protect customers and financial institutions in today’s increasingly digital world. By complying with AML legislation, banks protect themselves and therefore their customers from financial penalties, such as fines. Furthermore, these processes catch fraudsters early in the process of potential money laundering and stop them in their tracks, preventing illegitimate funds from entering circulation.

As more forms of digital, and therefore harder to regulate, currencies grow in their use and acceptance, it is important that AML legislation and processes keep pace in sophistication, ease of implementation, and ease of use for end customers. They must also provide a high level of security and assurance for financial institutions, making NFC First an ideal approach to AML.

How is AML applied in practice?

As previously mentioned, AML is applied practically through CDD and KYC processes. A robust set of processes should include:

- Transaction screening mechanisms (CDD)

- Verifying the identity of potential customers and reverifying them periodically (KYC)

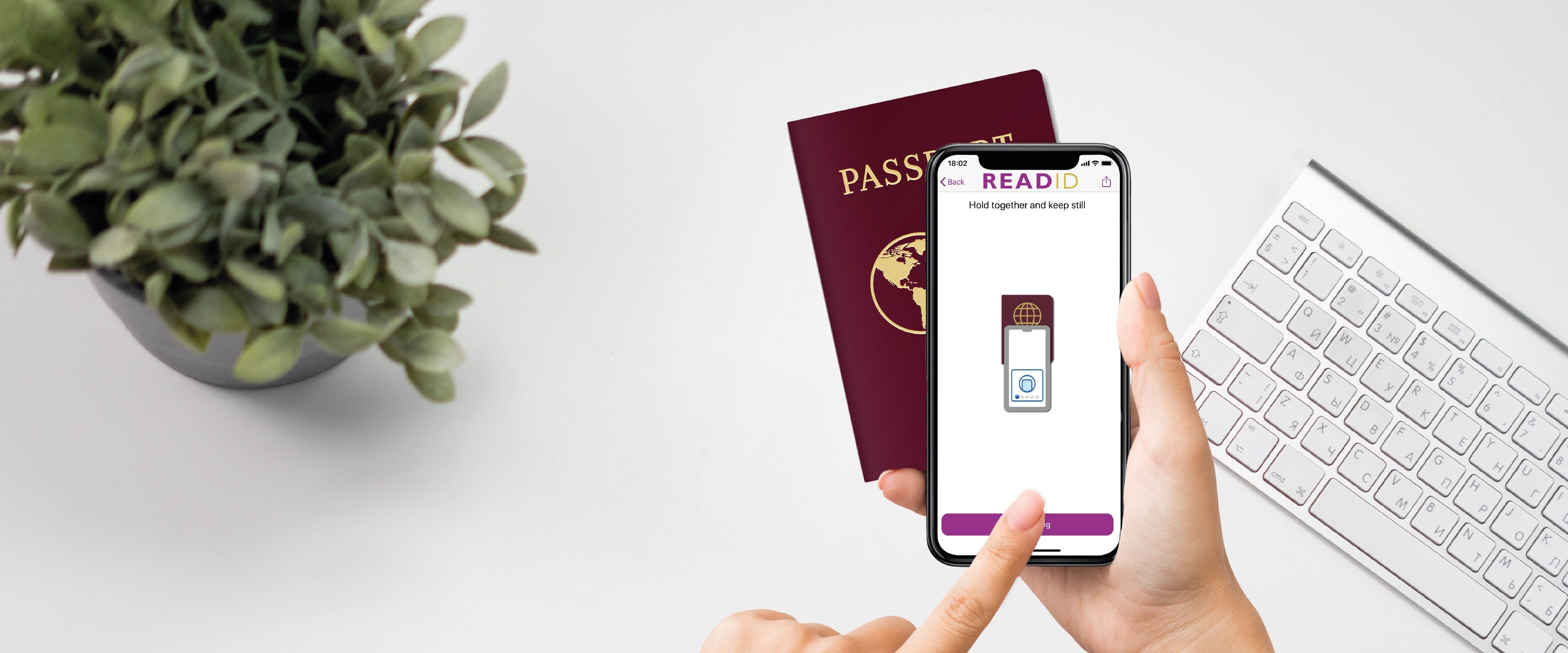

An example of these processes in practice is customer onboarding for ING in The Netherlands, where new customers are required to verify their identity when opening an account. This is achieved via the use of ReadID technology, which ING implemented into their own app. By using an electronic identity document such as a passport, identity card, or residence permit, ING customers can use their smartphone’s NFC capability to easily verify their identity and start mobile banking.

How can ReadID improve your AML compliance?

A cornerstone of AML compliance is having a secure set of Know Your Customer and Customer Due Diligence practices. But how do you as a financial institution maintain the highest level of security assurance while maintaining an enjoyable and speedy process for the end customer? The answer is simple; remote identity verification via a mobile application and NFC, made possible by ReadID. NFC by its very nature is highly secure, with document chips featuring many inherent security features, such as country signing certificates from issuing authorities for document authenticity checks, and NFC producing no reading errors that can be present in OCR verification methods.

All verification is done on ReadID’s secure cloud server, ensuring full compliance with privacy laws and directives such as GDPR, and keeping your customer’s data safe. There is also exceptional document and device coverage. ReadID is proven to work on over 2600 models of devices and as of 2022, 170+ countries produce electronic identity documents. Finally, ReadID not only provides compliance but also conversion- Rabobank saw their conversion almost double after implementing ReadID into their app.

ISO/IEC 27001 certified

ISO/IEC 27701 certified

eIDAS module certifications

SOC2 type 2

Cyber Essentials Plus